Hybrid Long-Term Care Life Insurance

Feel confident about protecting your retirement savings and assets.

What is Hybrid long-term care life insurance?

The unique guarantees of hybrid plans address the concerns of those who question “what if I never need long-term care.” Also known as combos or linked benefits, these plans link whole life or universal life insurance with long-term care coverage to:

- Pay for your long-term care services if you need care, or

- Pay your estate a tax-free life insurance benefit if you don’t need care, or

- Guarantee your money back if you change your mind and want to cancel your policy

They cover home health care, homemaker services, adult care homes and other assisted living arrangements, in addition to nursing homes.

Hybrids require more substantial premium to fund them, either in a single one-time payment or payments for up to 10 years. (One company will allow you to pay premiums over your lifetime.) Because you essentially “pay-up-front”, your premiums can never be subject to a rate increase.

Plan for Living.

It’s a fact of life today. As we continue to live longer, millions will face the prospect of needing or providing long-term care at some point in their lives. Long-Term Care plans help you to:

SHIELD ASSETS

Feel confident about protecting your retirement savings and assets

PROTECT FAMILY

Be proactive about reducing the burden of care that often falls on family members

TAKE CONTROL

Take control of your care decisions & maintain the independence to choose where you receive care

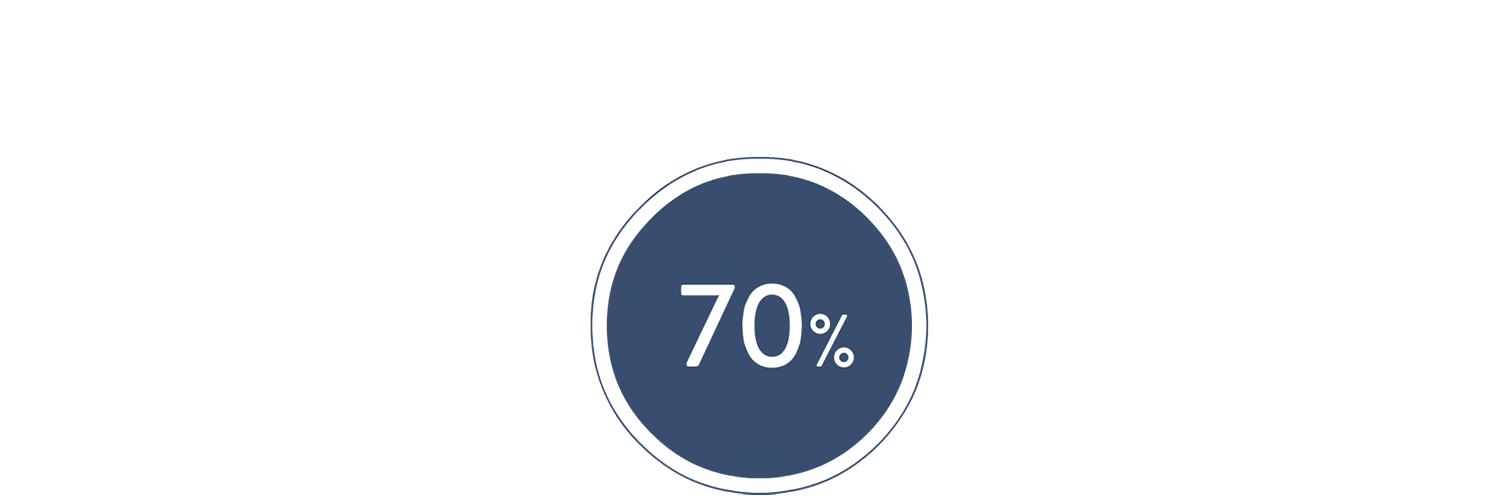

Who will need Long-Term Care?

70% of people age 65 can expect to use some form of long-term care services during their lives. For people with chronic diseases or family history, the chances are greater.

*U.S. Department of Health and Human Services (https://longtermcare.acl.gov/the-basics/who-needs-care.html)

The reality of living longer is that many will likely need long-term care in their lifetime, yet millions of people are continually caught in the following problematic cycle:

FINANCIAL BURDEN

While the costs for each type of care can vary greatly, they can add up quickly.

DEPLETE SAVINGS

Families can deplete their hard-earned life savings as they pay for this increasingly expensive care out of their own pockets.

LACK OF CHOICE + BURDEN TO FAMILY

Less funding = less power to choose how & where you receive your care, and the heavy financial and emotional burden falls to family members.

Meryl’s Story…

The reality of long-term care hits hard. Hear former broadcast journalist Meryl Comer’s personal story about caring for her husband, who was diagnosed with Alzheimer’s disease at age 57.

A clear solution, no matter your budget…

Long-term care insurance can help pay for care expenses and keep you in control of where and how you receive your care. It can be designed in any number of ways so that it fits your needs—and your budget.

Hear Rob Lowe, Maria Shriver, Angela Bassett & others have “The Talk” about long-term care planning…

Having the conversation with loved ones about long-term care and retirement planning can be tough. Join us in discussing the reality of aging and getting older, and how we can prepare for it.

Is is right for me?

You’ll want to consider long-term care insurance if you want to:

SHIELD ASSETS

Feel confident about protecting your retirement savings and assets

PROTECT FAMILY

Be proactive about reducing the burden of care that often falls on family members

TAKE CONTROL

Take control of your care decisions & maintain the independence to choose where you receive care

Meet Bob…

Hear Bob’s personal story on his experience with long-term care insurance.

When is the right time to buy?

When it comes to long-term care planning, there are two important reasons to address your future needs sooner rather than later:

The younger you buy, the lower the cost.

The cost of long-term care insurance is primarily based on your age and health when you apply for coverage. Therefore the younger and healthier you are, the lower your premium will be.

Unexpected accident or illness.

The coverage you buy for your future can also help protect you today. If an accident or illness were to occur when you were relatively young, which required you to need long-term care, owning a long-term care insurance policy would ensure you have coverage to help pay for the cost of care.

Why do some people find it so difficult to think about and plan for?

- Studies on aging in America show that we have a strong tendency to envision ourselves aging vibrantly and dying quickly, being physically active and clear thinking, virtually until our dying breath. But it is simply not true that we can know in advance how we ourselves will age and what we will feel about our life once we find ourselves not 45 and fit, but 75 and viewing life with a different lens.

- Unfortunately it is human nature to wait until there is a crisis to act. Priorities that are here today command our attention and dollars, and too many delay planning until it is too late.

- And finally, most Americans are bewildered about the subject of long-term care and so, they underestimate the cost of care and overestimate how much help they can expect from Medicare to pay for it.

“Better to have and not need, than to need and not have.”

Frequently Asked Questions

How is AgeWell different than other insurance websites?

Most every insurance website exists to generate leads for insurance agents. In other words, you tell them you’re interested and they turn you into a “Sales Lead” for agents to call to sell you something.

Our approach is different. We know that every person who expresses an interest is not necessarily ready or able to buy something. We consult and educate first, at no charge. Then, if its right for you and you think we’re a good fit, we’ll help you get the best plan for you and your budget.

Will I understand my plan if I don’t sit down with an agent, face-to face?

We’ve been in this business a long time and there were many years when we sat down across the kitchen table from our clients to educate them about their choices and walk them through the application process. Today, through the power of technology, we have created a simpler method for you – one where you can stay in the comfort of your own home for the entire process.

We’ll walk you through each detail, every step of the way. Using screen-sharing technology, all you’ll do is click your mouse, and you’ll automatically see you adviser’s computer screen, where you will be walked through plan comparisons and options, covering every detail that would be explored in a face-to-face meeting. We find that our customers enjoy this process because it is easy, straight-forward, and a whole lot less time consuming than the old-fashioned way. We’ve thoughtfully engineered the experience to make it quick, convenient and frustration-free for you so that you can get back to enjoying your life, except now with the safety and satisfaction that your future, your assets and your family are protected.

Do I have to pass a health test to get a long-term care plan?

Not exactly. When you apply, the insurance company will conduct a personal interview with you by telephone or in-person. Most companies will also order your medical records from your doctor. What they see in your medical records, together with the results of your personal interview, determines if you will be approved for a plan.

Am I too young or too old for a long-term care plan?

You qualify for this protection with your good health, no matter your age. Mostly, people put their long-term care plan in place between ages 45 – 60 when their health is still good enough to qualify. Often, when people wait until their 60’s, they may already have too much negative medical history accumulated to qualify for a plan.

How much does a long-term care plan cost?

The typical annual premium is much less than paying for one month of long term care services out of your pocket.

What is the difference between traditional standalone long-term care insurance and hybrid long-term care life insurance?

Traditional standalone long-term care insurance works like your auto, homeowners, and health insurance. You pay your premium monthly, quarterly, semi-annually, or annually to keep your policy in force. There is no cash value. You receive the tax-free benefits to pay for your long-term care services when you file a claim. Your premium may be subject to a rate increase in the future, but only if your State permits it. Because you “pay-as-you-go,” these plans are more affordable. They offer more flexibility at claim time and waive your premium when you are receiving care. They offer appealing coverage options such as Shared Care for couples, may be certified under your State’s Partnership for Long-Term Care Program to protect your assets, and for business owners, premiums are tax deductible.

Hybrid long-term care life insurance links whole life or universal life insurance with long-term care coverage to: 1) pay for your long-term care services if you need care, or 2) pay your estate a tax-free life insurance benefit if you don’t need care, or 3) guarantee you can receive your money back if you change your mind and want to cancel your policy. These hybrids require more substantial premium to fund them up-front, either in a single one-time payment or payments for up to 10 years. (One company will allow you to pay premiums over your lifetime.) Because you essentially “pay-up-front”, your premiums can never be subject to a rate increase. Typical ways to fund these are by exchanging the cash value from an existing life insurance policy or repositioning a liquid asset such as a CD (Certificate of Deposit).

What are Long-Term Care Partnership Policies?

Practically every state in the nation has a Long-Term Care Partnership Program. It is a partnership between your state government and private insurance companies. Insurance companies voluntarily agree to participate by offering long-term care insurance policies that meet your state’s specified criteria. The state agrees to provide Medicaid (Medi-Cal in California) asset protection to people who purchase partnership-qualified policies.

Do traditional standalone long-term care insurance premiums go up?

Rates do not go up as you get older. Rates do not go up if you file a claim. Your rates are fixed at the age that you buy the policy. The only way that your rate can go up is if your State approves a rate increase on all policies for everyone who owns that policy series. If that is the case, you will have the ability at that time to either accept the rate increase or lower your benefits to maintain your original rate.

Do hybrid long-term care life insurance premiums go up?

No, never.

Why do I need a long-term care plan? I’m never going to go to a nursing home.

When it was first introduced over forty years ago, long-term care insurance was marketed as nursing home insurance. That is why often times it is still misunderstood. Today’s long-term care plans encompass a broad variety of treatment and care-giving options, such as home health care, homemaker services, adult care homes and other assisted living arrangements, in addition to nursing homes. They also contain provisions to adapt as technology changes so that they cover the care capabilities that will be available 30-40 years from now. Most people receive long-term care in settings outside of a nursing home. Today more than 70% of long-term care policyholders are using their plans to be cared for in the comfort of their own home.

What should I be prepared to discuss to begin looking into long-term care planning?

Being thorough and candid about your health history is the most important first step. The better we know this, the better we can help you. Not every company will take every medical condition. Some are better for certain conditions than others. Our years of experience and relationships with Underwriters at all of the companies allows us to guide you to the best company with the best chance for your approval.

I think I’m already covered for this, aren’t I?

Many people think (or hope) that the other insurances they have will pay for long-term care but here is the reality:

- your group health insurance or your HMO has no coverage for long-term care

- long term disability doesn’t pay for long-term care; it pays for your lost income

- Medicare doesn’t cover the day-to-day personal care assistance you need if you are unable to take care of yourself

Let’s get started!

Call us now at (888) 243-1770 and one of our advisers will be in touch with you very shortly